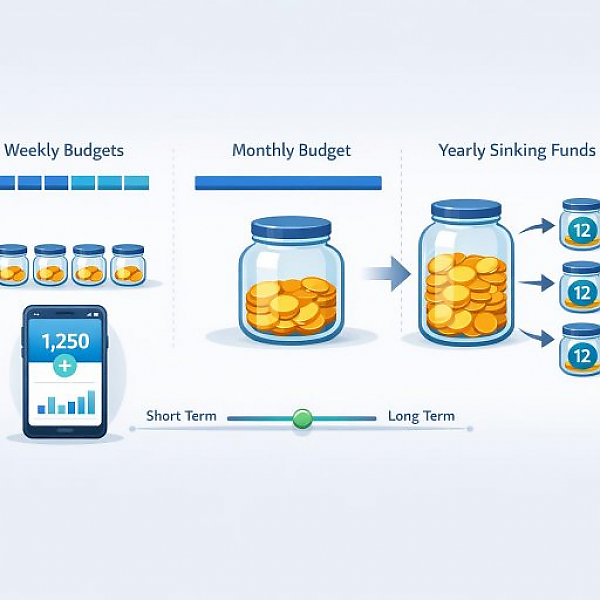

Budget periods indicate the time span for which you plan and analyze your income and expenses—for example, per week, per month, or per year; the budget period you choose determines how precisely you can manage spending and how clear your reports are in a digital budget planner.

In a digital budget planner like MyMicroBalance, you can choose different budget periods for different categories. The following table shows a comparison, typical use cases, pros and cons, and simple euro examples for conversion.

| Budget period | Definition & typical use | Pros / cons & euro examples |

|---|---|---|

| Weekly budget | Definition: You set a fixed amount per week. Each calendar week has its own limit. Typical use:

| Pros:

Cons:

Examples:

|

| Monthly budget | Definition: You plan your income and expenses per calendar month. This is the most common budget period. Typical use:

| Pros:

Cons:

Examples:

|

| Yearly budget | Definition: You look at income and expenses over an entire year. This is suitable for infrequent or irregular payments. Typical use:

| Pros:

Cons:

Examples (convert to monthly):

|

Choosing a budget period depends on how regular a payment is and how tightly you want to control it:

A simple rule of thumb: The harder an expense is to keep an eye on, the shorter the budget period should be (e.g., week instead of month).

The following steps will help you structure your budgets sensibly in a digital budget planner like MyMicroBalance.

So that large annual costs don’t catch your account off guard, break them down into manageable monthly amounts.

Examples:

For flexible everyday expenses, you can work with weekly or monthly limits.

Example: You spend an average of €320 per month on groceries. With a weekly budget, you plan €320 ÷ 4 = €80 per week as your limit.

After one to three months, you should check whether your budget periods fit your daily life.

With clearly chosen budget periods, your digital budget planner becomes more structured, and you’ll spot early whether you’re staying within your plan or need to make adjustments.

1

1 2

2 3

3 4

4